The Power of a Written Financial Plan for Physicians

Most physicians spend over a decade in training, learning how to diagnose disease, perform procedures, and stay up to date on the latest medical literature. Yet ask even a seasoned doctor about their personal financial plan, and the response is usually… silence.

It’s not that physicians don’t care about money. They do. But after years of delayed gratification, six-figure student loans, and long hours, many doctors fall into the trap of “I’ll figure it out later.” Later often turns into never.

That’s why a written financial plan is so important. It’s not glamorous, but it’s the foundation of long-term wealth — the same way a treatment protocol helps guide consistent medical decision-making.

Why Doctors Need a Financial Plan

Doctors earn high incomes, but high income does not automatically equal high net worth. In fact, many physicians live paycheck to paycheck despite making $250,000+.

The reasons are obvious:

-

- Student loans that rival mortgages.

-

- Lifestyle inflation (“I’ve worked hard, I deserve the car/house/vacation”).

-

- Lack of structure around saving, investing, and protecting income.

A written plan solves these problems by serving as your roadmap. Just as you wouldn’t enter the OR without a protocol, you shouldn’t approach money without one.

What Goes Into a Financial Plan?

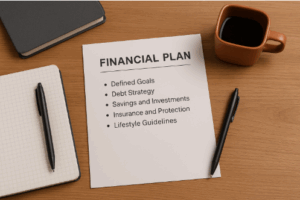

Your plan doesn’t need to be a 50-page binder. In fact, shorter is better — easier to follow, easier to update. Think of it as a one-page guideline covering the following areas:

1. Defined Goals

What do you want your money to do for you? Retire at 55? Pay off loans in 5 years? Buy a vacation home? Naming your goals makes them real.

2. Debt Strategy

Will you refinance your student loans or pursue PSLF? Are you comfortable with a mortgage that’s 2x your salary, or do you want something smaller? Decide before emotions take over.

3. Savings and Investments

What percentage of your gross income will you save? (Hint: 20% is a strong starting point.) How will you allocate across 401(k), Roth IRA, taxable accounts, or real estate?

4. Insurance and Protection

Do you have own-occupation disability insurance? Adequate life insurance if you have dependents? Umbrella coverage? Your plan should answer these before you need them.

5. Lifestyle Guidelines

Yes, this belongs in your plan. How much will you allow for cars, travel, dining out? Explicit guardrails prevent lifestyle creep from taking over.

First Steps to Create Your Plan

If you’re new to this, don’t get overwhelmed. Start simple.

-

- Write down your top three priorities (example: pay off loans, save for retirement, build college fund).

-

- Assign a timeline and rough dollar amount to each.

-

- Commit to a basic savings rate (like 20% of gross income).

-

- Put it all in writing. Doesn’t matter if it’s a Google Doc, a notebook, or the back of a napkin. If it’s written down, it counts.

Common Mistakes to Avoid

-

- Waiting for perfection

Your plan will evolve. Don’t delay because you don’t know every detail today.

- Waiting for perfection

-

- Copying someone else’s plan

Your situation, goals, and values are unique. Use others as inspiration, but write your own prescription.

- Copying someone else’s plan

-

- Failing to update

Life changes — new jobs, kids, house, practice buy-in. Update your plan annually (or when a major event happens).

- Failing to update

The Doctor Analogy

Think about how you practice medicine. When a patient comes in, you don’t wing it. You take a history, make a diagnosis, write a treatment plan, and follow up.

Your financial life deserves the same approach. Without a plan, you’re just reacting to symptoms (a high tax bill, a bad investment, a big monthly payment). With a plan, you’re proactively managing your financial health.

Final Thoughts

A written financial plan doesn’t have to be intimidating. It can fit on one page, and it should reflect your goals, your values, and your priorities.

The doctors who build wealth and live with less stress aren’t necessarily the ones with the highest salaries or the flashiest portfolios. They’re the ones who took the time to write down a plan and stick to it.

So grab a pen, open a document, or scribble on a napkin. Your future self will thank you.